Key Takeaways

Outlet spend moved from cash to company-funded UPI wallets. Every store now runs its day-to-day expenses through a CashBook UPI wallet instead of physical petty cash, so company money leaves the business only as a recorded UPI payment.

Local contractors and suppliers are paid the same way, now fully tracked. Most outlet payments go to individuals such as maintenance contractors, daily-wage labour and vegetable or grocery suppliers who accept personal UPI. Payments that were once invisible are now logged automatically.

Control stayed central while spending power moved to the ground. Outlet and area teams pay vendors the moment a store needs it, while the finance team keeps caps, approval rules and a live view of every rupee.

Bills and categories are captured at the point of payment. Mandatory bill attachment and near-total categorization give finance audit-ready records without anyone chasing receipts at month end.

The model scales with new outlets. Adding a store simply means adding a wallet, so expense control grows with the chain instead of slowing it down.

About Company

About WOW! Momo

WOW! Momo is India's largest homegrown quick service restaurant chain. It began in 2008 as a small momo brand started by Sagar Daryani and Binod Homagai in Kolkata, and has since grown into a multi-brand QSR group operating more than 850 outlets across 95+ cities. Today the company runs four brands, Wow! Momo, Wow! China, Wow! Chicken and Wow! Kulfi, and serves customers from high streets, malls, food courts and even outlets located at IOCL petrol pumps.

That scale is exactly what makes outlet expense management hard. A QSR chain does not have one office where everyone spends and submits bills at the end of the day. It has hundreds of kitchens and counters spread across tier-1, tier-2 and tier-3 cities, each one generating a steady stream of small, time-sensitive payments to keep the store running. A leaking tap, a refilled gas cylinder, a vegetable delivery, an electrician, a cleaning vendor. Individually these are tiny amounts. Across a multi-outlet network they add up to thousands of transactions a month, and traditionally most of them moved as cash.

Managing this distributed petty cash across a fast-growing chain is what brought Wow Momo to CashBook.

Challenges

Why outlet expenses are the hidden challenge in QSR growth

India's quick service restaurant sector is one of the fastest-growing parts of the economy. The country is home to more than 500,000 QSR outlets, and the organised, chained segment alone now runs into the tens of thousands of stores, expanding quickly into smaller cities. Every new outlet adds revenue, but it also adds a new node of daily spending that the finance team back at head office has to somehow see and control.

Most of this spending happens through UPI. India now has over 65 million merchants accepting UPI, and person-to-merchant payments make up the majority of transaction volume, according to NPCI data. For a QSR chain, that is both an opportunity and a problem. Staff can pay almost any vendor instantly, but when they pay from personal accounts or a cash box, the company loses visibility of where its money actually goes. The challenge for a multi-outlet QSR is not whether to use UPI, it is how to make UPI spending company-funded, controlled and audit-ready.

This is the gap Wow Momo set out to close. Leadership wanted to take cash out of a multi-outlet business, run every outlet on one platform, and make outlet spending audit-ready at the scale of hundreds of stores and growing. The story below shows how a large QSR chain went from cash-driven outlet operations to a fully digital, controlled expense system using CashBook UPI wallets, and why the same approach works for almost any multi-outlet restaurant brand.

What expense challenges do multi-outlet QSR chains face?

Before CashBook, Wow Momo managed outlet expenses the way most growing restaurant chains do, with cash floats and after-the-fact reimbursement. Head office would push money to outlets or to managers, store staff would spend it on whatever the outlet needed that day, and the paperwork would catch up later, if at all. For a single store this is workable. Across a network of hundreds of outlets in dozens of cities, it quietly turns into one of the biggest operational and financial risks in the business.

The first problem is the nature of QSR spending itself. Outlet expenses are high in frequency and low in value. A busy store can make dozens of small payments in a month, and across a chain that becomes thousands of transactions. The biggest single category for most multi-outlet QSR chains is outlet repair and maintenance, things like plumbing, electrical work, equipment servicing and small fit-out fixes, followed by supplies, local conveyance, cleaning, diesel for gensets, water and staff welfare. A large share of these payments go to individuals, not to organised merchants with proper invoices. Local contractors, daily-wage workers and neighbourhood vegetable or grocery suppliers all expect to be paid on the spot, usually into a personal UPI ID.

That creates the second problem: visibility. When a store manager hands cash to a contractor or pays a supplier from a personal account, there is no clean digital record tied to the company. Finance cannot see, in real time, what a given outlet has spent or on what. Bills for repairs and supplies are paper, and paper gets lost, faded or forgotten on the way from the outlet to head office. By the time month-end arrives, the finance team is reconstructing each outlet's spending from memory, WhatsApp messages and whatever receipts survived.

The third problem is cash itself. Floats sitting in hundreds of outlets mean company money is scattered across the network with no view of how much is left or whether it was used as intended. Store staff often end up spending their own money first and waiting days to be reimbursed, which is a constant source of friction for the people actually running the outlets. And because spend is concentrated in evening service hours, when head office is closed, the money moves precisely when oversight is weakest. The result is the worst combination for a finance team in a multi-outlet business: real money moving fast, with records arriving slow.

The core challenges Wow Momo needed to solve were:

Store staff paid vendors from personal cash or UPI, then waited days for reimbursement.

Payments to individual contractors and local suppliers left almost no usable digital trail.

Paper bills for repairs and supplies went missing before they reached finance.

Cash floats sat idle across hundreds of outlets with no real-time visibility of balances.

Month-end reconciliation meant rebuilding each outlet's spend from memory and scattered receipts.

None of these issues is unique to Wow Momo. Any restaurant chain that crosses a few dozen outlets runs into the same wall: the spending happens at the edge, in the outlets, but the control sits at the centre, in finance, and cash leaves a gap between the two. Closing that gap, without slowing down the stores, was the real brief.

Solutions

How CashBook solved WOW! Momo's multi-outlet expense problem

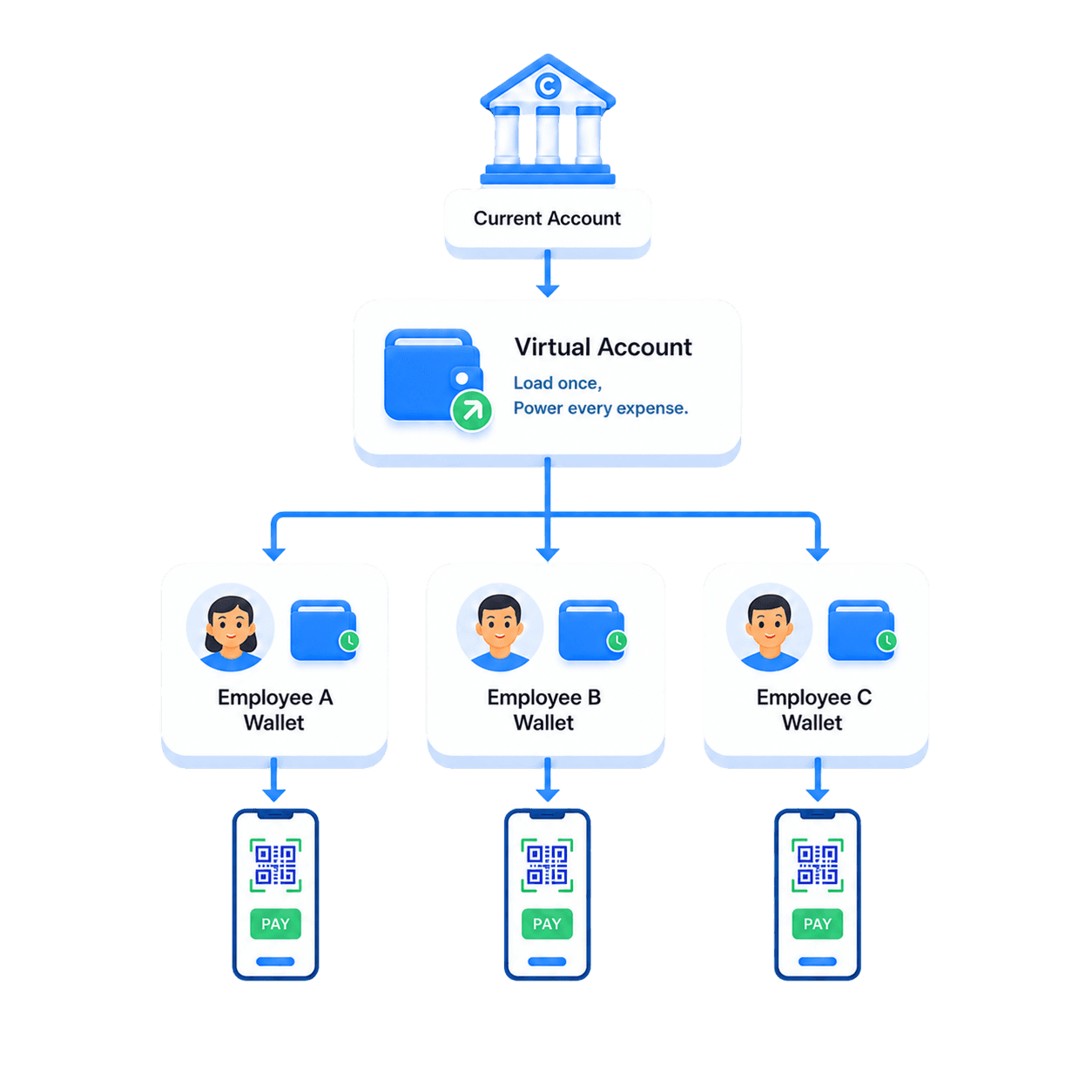

WOW! Momo moved its outlet spending onto CashBook UPI wallets. CashBook is an NPCI-certified, RBI-licensed, UPI-native expense management platform built around company-funded UPI wallets (CashBook UPI wallets). The idea is simple but powerful: instead of giving outlets cash, the company gives each outlet a wallet loaded with company money. Staff pay vendors by UPI exactly as they always did, but now the money is the company's, the control is the company's, and every payment is recorded the instant it happens.

A master account is loaded centrally, and finance distributes funds into individual outlet and area wallets. Because the money is pushed from the centre, there is no need for staff to front their own cash and no loose float sitting in a drawer. Each wallet can carry limits, so a small outlet wallet behaves like true petty cash while a busier cluster or maintenance wallet has more room, all decided by finance rather than by whoever is holding the cash. Every vendor the chain already paid, the plumber, the vegetable supplier, the cleaning service, already accepted UPI, so CashBook slotted into existing vendor relationships without changing a single one. The payment method stayed the same. The control around it changed completely.

The part that mattered most for a chain of this size was governance. Wow Momo wanted spending to be controlled by policy, not by trust. CashBook gave them mandatory bill attachment, so a payment has to carry its bill or the wallet pauses until it does, near-total categorization so every rupee is tagged to a spend type, and a department-based, multi-tier approval engine that routes payments by amount and by team. Small everyday payments clear automatically, while larger maintenance or procurement payments route to the right approver. Combined with employee profile tagging by store, department and role, finance can attribute spend down to the individual outlet and see the whole chain in one live dashboard.

Funding also became deliberate rather than reactive. Instead of parking large buffer balances in stores, finance tops up outlet wallets on a regular schedule and adds capacity in seconds from the dashboard when a store needs it, which keeps idle cash low while making sure no outlet is ever stuck waiting for money. Nobody fronts personal cash, so the out-of-pocket reimbursement cycle that frustrates store staff disappears entirely. And because each payment carries its bill, category and outlet tag the instant it happens, the same system that controls spending also produces the records, so finance is not collecting paperwork after the fact, it is reviewing data that is already complete.

In practice, the solution came down to five building blocks:

Company-funded UPI wallets for every outlet and area team.

Mandatory bill attachment on every payment.

Automatic categorization of outlet spend at the time of payment.

Department-based, multi-tier approval workflows.

Employee profile tagging and a real-time dashboard.

The design resolves the central tension in any multi-outlet operation, the trade-off between control and speed, by separating the two. Outlets keep the autonomy to pay a vendor the instant a store needs it, and finance keeps oversight, limits and a complete ledger. CashBook became the single source of truth for outlet spending across the network.

Impact

What changed after WOW! Momo moved to CashBook?

Within months of rolling out across the chain, the way money moves through Wow Momo's outlets looked completely different. The shift from cash to company-funded UPI wallets did not just digitise payments, it changed what the finance team could see and control. Thousands of small outlet payments that used to disappear into cash and lost receipts now arrive as structured, categorized, bill-backed records in real time. The change was not gradual either. Once an outlet switched to a wallet, its spending became visible from the first transaction, so the benefit landed the moment each store came online rather than after a long settling-in period.

The most visible change is transparency. Every outlet transaction is now captured with the payee, amount, time, category and outlet, including the large share of payments that go to individual contractors and local suppliers. The biggest blind spot in QSR expense management, payments to people rather than to organised merchants, became fully auditable. At the same time, store staff stopped using their own money. There are no reimbursement claims to file and no waiting for personal cash to come back, which removed a real source of friction for the people running the outlets.

Control improved as much as speed. With wallet limits, enforced bill attachment and policy-based approvals, the gaps where petty cash leakage usually hides simply close up. Because records carry GST-ready vendor details, the chain also protects input tax credit that undocumented cash spending tends to forfeit.

Cash exposure dropped at the same time. With funds pushed to wallets just in time instead of left as floats in stores, far less company money sits idle across the network at any moment, and finance can see exactly where every rupee is. Month-end also stopped being a reconstruction project. Instead of rebuilding each outlet's spend from receipts and messages, finance now reviews complete records that are already tagged by store and category, so closing the books is a quick check rather than an investigation. The headline outcomes were:

Every outlet transaction is now digitally recorded, with payee, amount, time, category and store captured automatically.

Previously invisible payments to individuals became fully auditable, closing the biggest gap in QSR expense tracking.

Out-of-pocket spending and reimbursement claims were removed for store staff, who now pay directly from company wallets.

Idle cash float across outlets dropped sharply, because funds are pushed just in time instead of parked in stores.

Month-end reconciliation became a review, not a reconstruction, with audit-ready, GST-friendly records available on demand.

The deepest change is structural. Finance moved from reconstructing the past to reviewing the present, and the same wallet infrastructure that runs today's outlets will absorb the next hundred stores without adding administrative overhead. For a chain that is still expanding into new cities, that is the difference between expense control that fights growth and expense control that enables it.

Industry Application

Which businesses around QSR benefit most from CashBook?

WOW! Momo's challenges are not specific to one brand or even to momos. Any food and beverage business that operates more than a handful of locations runs into the same pattern: high-frequency, low-value outlet spending, a lot of it paid to individuals, happening far from the finance team. CashBook is built for exactly this kind of distributed, on-the-ground spending, which makes it a strong fit across the wider QSR and multi-outlet food ecosystem.

Quick service restaurant chains.

Run repair, supplies, conveyance and utility spend across every outlet through capped, bill-backed UPI wallets with outlet-level visibility.

Cloud kitchens and delivery-first brands.

Give each kitchen a wallet for ingredients, packaging, gas and small repairs without handing out cash.

Casual dining and restaurant groups.

Control multi-location kitchen and front-of-house spend from one dashboard while letting each outlet pay vendors instantly.

Cafe, bakery and dessert chains.

Manage daily supplier and maintenance payments across a fast-growing store network with audit-ready records.

Food court and franchise operators.

Distribute spending authority to individual counters or franchisees while keeping central caps and approvals.

Catering and institutional food services.

Equip site and event teams with wallets for on-ground purchases instead of cash advances and reimbursements.

The pattern WOW! Momo proved applies to any multi-outlet operator: if your spending happens at the edge, your control should too. To see how the same wallet model works in other distributed businesses, look at how Urban Vault runs multi-center office spend and how HopCharge manages field and fleet payments, both on the same company-funded UPI wallet structure.

Frequently Asked Questions

How do QSR chains manage petty cash across multiple outlets?

Most QSR chains start with cash floats and after-the-fact reimbursement, where head office pushes money to outlets and reconciles later. This breaks down at scale because spending is high-frequency and largely paid to individuals. CashBook replaces it with company-funded UPI wallets that carry limits, enforce bill attachment and route approvals by policy, so outlets pay vendors instantly while finance keeps central control and a live ledger.

Can UPI wallets be used for restaurant outlet expenses like repairs and supplies?

Yes. Repair contractors, equipment vendors, vegetable and grocery suppliers and cleaning services almost all accept UPI, so CashBook wallets pay them directly without changing any vendor relationship. Every payment captures the vendor, amount, time and category automatically, and a bill can be attached at the moment of payment for audit-ready records.

How does CashBook give finance teams outlet-level expense visibility?

Each wallet is tagged by store, department and role, and every payment lands in the ledger instantly with its category and bill. Finance sees spending across all outlets from one dashboard in real time, instead of reconstructing each location's spend from receipts at month end.

Conclusion

WOW! Momo built one of India's largest QSR networks by opening outlets fast across the country. CashBook extends that same discipline to the money that keeps each outlet running: the repair vendor at a live store, the vegetable supplier in the morning, the electrician during evening service. Spending that used to move as untracked cash and surface weeks later now flows instantly through capped, bill-backed UPI wallets and lives in one real-time ledger across every city the brand operates in.

For any multi-outlet QSR, the lesson is simple. You do not have to choose between letting outlets move fast and keeping finance in control. Company-funded UPI wallets give you both: instant spending power at the outlet and complete visibility at head office, with audit-ready records by default.

Book a demo to see how the same multi-outlet expense management setup used by WOW! Momo can work for your restaurant chain, cloud kitchens or franchise network, or write to us at support@cashbook.in.