What Is e-RUPI? Understanding NPCI's Digital Voucher System

e-RUPI represents a significant innovation in India's UPI expense management ecosystem. Launched by the National Payments Corporation of India, it functions as a prepaid, purpose-specific digital voucher designed for targeted benefit distribution.

How e-RUPI Works: Technical Architecture

The e-RUPI workflow operates through these stages:

Voucher Issuance: Businesses integrate with authorized e-RUPI providers and generate vouchers linked to their bank accounts

Restriction Layer: Each voucher is locked to specific merchants or Merchant Category Codes (MCCs)

Employee Redemption: Recipients add vouchers to their UPI apps (Google Pay, PhonePe, Paytm)

Payment Authorization: Transactions succeed only at enabled P2M (Person-to-Merchant) touchpoints

Unlike traditional expense management software, e-RUPI creates a closed-loop system where funds remain in business accounts until redemption occurs.

The Core Promise: e-RUPI Advantages for Business Expense Management

1. Zero Employee KYC Requirements

e-RUPI eliminates employee onboarding friction entirely. Businesses can distribute vouchers without waiting for employees to complete Know Your Customer formalities; a significant advantage for quick benefit distribution programs.

2. Category-Specific Spend Controls

The MCC-based restriction system enables precise allocation:

Fuel-only vouchers for field sales teams

Medical expense vouchers for healthcare reimbursements

Education vouchers for training programs

Food & beverage vouchers for employee welfare

This granular control aligns with expense approval workflows many finance teams require.

3. Treasury Management Benefits

Funds remain locked in company bank accounts until employees redeem vouchers. This "just-in-time" disbursement model improves working capital management and provides clearer cash flow visibility compared to traditional petty cash management systems.

Critical Operational Limitations: Why e-RUPI Struggles in Real-World Corporate Environments

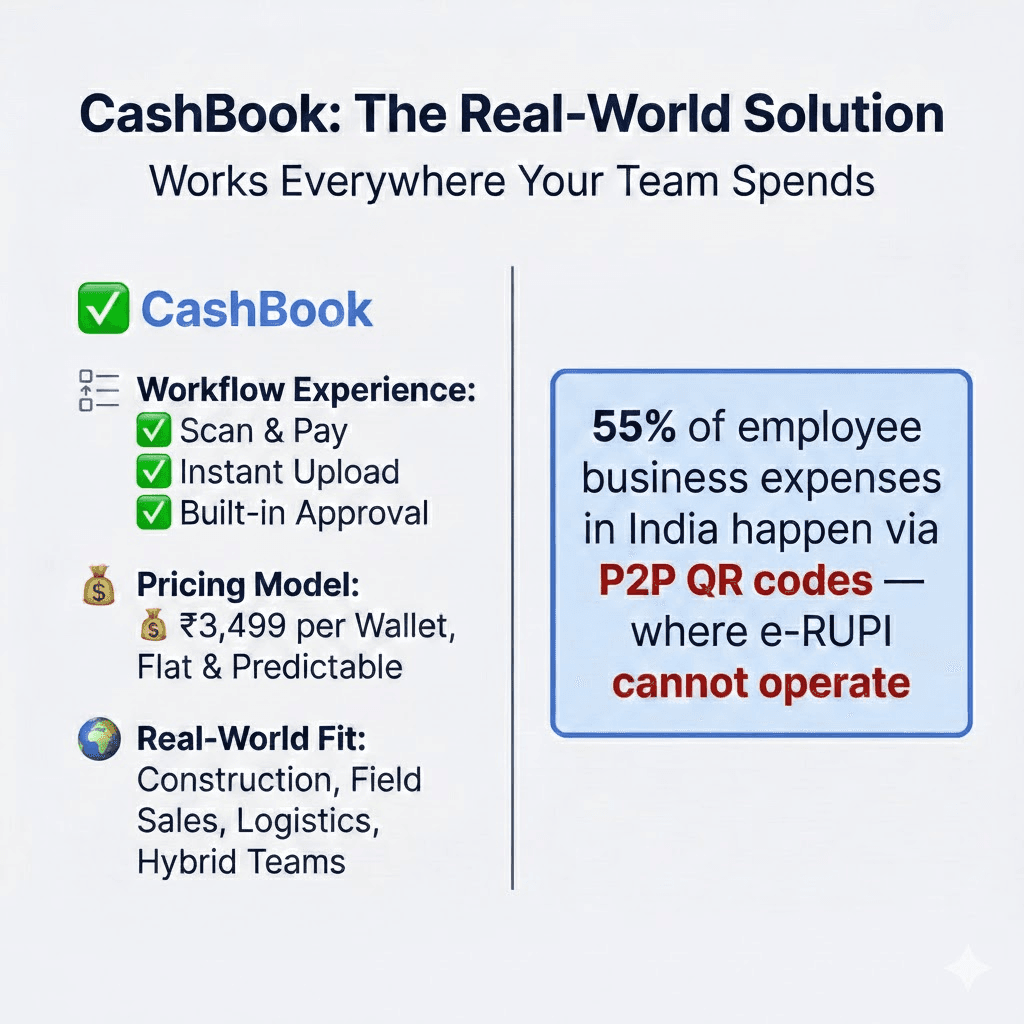

Limitation 1: P2M-Only Architecture Creates a 55% Acceptance Gap

This is the most significant structural constraint.

Our transaction analysis across Indian businesses reveals:

55% of employee business expenses occur on P2P QR codes

Only 45% happen at formal P2M merchant terminals

Why P2P Dominates India's Business Spending Ecosystem

India's merchant ecosystem remains hybrid, with millions of vendors operating informally:

Real-World P2P Payment Scenarios:

Local hardware stores use personal UPI IDs

Auto-rickshaw and taxi drivers accept payments via personal QR codes

Construction site vendors transact through P2P channels

Small grocery shops and stationery suppliers rely on personal accounts

On-demand services (plumbers, electricians) use P2P exclusively

For field teams, sales executives, and site managers, more than half of legitimate business expenses become ineligible for e-RUPI payment. This creates operational friction, forces employees to seek reimbursements through separate channels, and undermines the efficiency gains e-RUPI promises.

Learn more about how to make business expenses through UPI compliantly.

Limitation 2: Merchant Enablement Is Not Guaranteed

Even formal merchants with P2M QR codes may not accept e-RUPI. The system requires:

Bank-Side Enablement: The merchant's acquiring bank must support e-RUPI transactions

Merchant Onboarding: Explicit enrollment for e-RUPI acceptance

Category Mapping: Correct MCC classification in banking systems

Practical Impact: Your employee arrives at a legitimate petrol pump with a fuel voucher; only to discover the transaction fails because the pump's bank hasn't enabled e-RUPI processing.

This creates unpredictable acceptance issues that damage employee experience and operational reliability.

Limitation 3: MCC Classification Inconsistencies Across Indian Banks

In theory, restricting vouchers by Merchant Category Code sounds powerful. In practice, India's banking ecosystem suffers from inconsistent merchant categorization:

Documentation Examples:

Petrol pumps incorrectly mapped under "hospitality" or generic retail

Travel agencies classified as "professional services"

Medical stores tagged as "general merchandise"

Category variations between acquiring banks

When your fuel-restricted voucher fails at a petrol pump categorized under the wrong MCC, your employee faces real-world business disruption. This isn't a rare edge case; it's a systemic classification problem across India's merchant network.

Limitation 4: Transaction Limits Create Administrative Overhead

Current implementations cap individual e-RUPI vouchers between ₹10,000–₹50,000 (exact limits vary by provider). For businesses managing substantial operational expenses:

Large equipment purchases require multiple voucher splits

Vendor payments exceeding limits need fragmented transactions

Project-based expenses create administrative complexity

Compare this to employee wallets for expenses, which handle flexible transaction sizes without arbitrary caps.

Limitation 5: Bank Dependency Restricts Accessibility

e-RUPI availability remains limited to specific banking partnerships:

Account Requirements: Often restricted to current accounts with particular banks

Integration Complexity: Deep technical connections required with bank systems

Regional Bank Challenges: Cooperative banks and smaller institutions may not offer access

Growing businesses need bank-agnostic expense management solutions that don't lock them into specific banking relationships.

Limitation 6: Extended Implementation Timelines

Because e-RUPI ties directly to business bank accounts, deployment involves:

Detailed compliance reviews

Technical integration with banking APIs

Multi-party approvals across financial institutions

Extended testing periods

For rapidly scaling operations, 6-8 week implementation cycles create significant opportunity costs. Modern corporate expense tracking solutions should activate within days, not months.

Limitation 7: Fragmented Documentation Workflows

The typical e-RUPI experience splits user workflows:

Payment happens in the employee's UPI app (Google Pay, PhonePe, etc.)

Invoice upload occurs in a separate provider application

Expense reporting flows through yet another system

This fragmentation leads to:

Missing receipts and documentation gaps

Delayed compliance validation

Manual follow-up overhead for finance teams

Poor visibility into real-time spending

Effective expense claim systems unify payment, documentation, and approval in one seamless experience.

Limitation 8: Percentage-Based Pricing Becomes Expensive at Scale

Most e-RUPI implementations charge 0.5%–0.7% of gross transaction value. While this appears reasonable initially, costs scale linearly with business growth:

Cost Projection Example:

Annual spend: ₹5 crore

Provider fee: 0.5%

Annual cost: ₹2.5 lakh

As your business scales to ₹20 crore in annual expenses, you're paying ₹10 lakh purely in transaction fees. This unpredictable cost structure makes small business expense management budgeting challenging.

Why e-RUPI Excels for Targeted Benefits; But Struggles for Employee Expenses

e-RUPI demonstrates clear value in specific use cases:

Ideal Applications:

Government scholarship distribution with controlled redemption

Corporate welfare benefits (gym memberships, health insurance)

Vendor-locked payments to specific service providers

Subsidy programs requiring purpose restrictions

Poor Fit for Corporate Expense Management:

Distributed field teams making diverse purchases

Dynamic vendor networks with informal payment acceptance

High-frequency, variable business spending

Operational environments requiring P2P payment flexibility

The fundamental mismatch lies in e-RUPI's design philosophy: it optimizes for restriction and control over operational flexibility and universal acceptance.

How CashBook UPI Wallets Solve Critical e-RUPI Limitations

CashBook emerged from understanding real business needs in India's hybrid payment ecosystem. After analyzing transaction patterns across diverse industries, we designed a UPI expense management solution that balances control with operational reality.

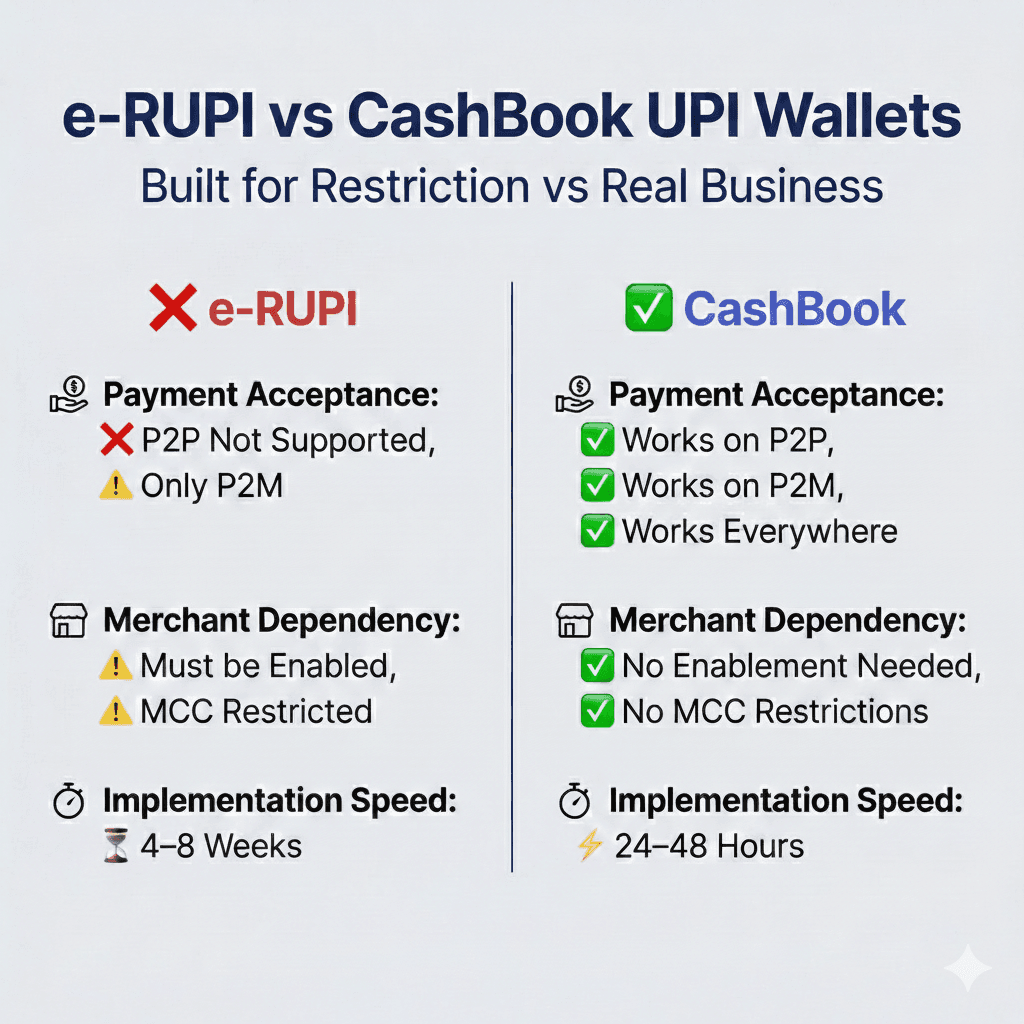

Solution 1: Universal Payment Acceptance (P2P + P2M)

The Core Differentiator: CashBook UPI Wallets work everywhere UPI is accepted; including the majority of business expenses occurring on P2P channels.

Employees can transact with:

Any merchant QR code (formal or informal)

Personal UPI IDs and phone number-based payments

All merchant categories without MCC restrictions

Zero dependency on merchant enablement status

This eliminates the acceptance friction that plagues e-RUPI implementations. Your employees focus on business activities rather than worrying whether payment will succeed.

Discover how businesses manage travel and expense management without acceptance barriers.

Solution 2: Admin-Controlled Limits Replace Merchant Restrictions

Instead of restricting where money can be spent, CashBook implements smarter governance:

Control Mechanisms:

Individual wallet balance limits per employee

Daily transaction caps to prevent overspending

Caps on number of transactions per day

This approach recognizes that finance teams need spending governance, not operational restriction. Employees gain flexibility while admins maintain oversight.

Solution 3: Rapid Deployment (24-48 Hours)

CashBook's bank-agnostic architecture enables swift activation:

Business KYC verification (standard regulatory requirement)

Virtual account created for business

Admin funds virtual accounts using simple bank transfer

Later, employee UPI wallets are funded using the funds in virtual accounts

Employees start transacting immediately

No complex banking integrations. No multi-week approval cycles. No merchant enablement dependencies.

For businesses needing quick solutions, this dramatically accelerates expense approval system implementation.

Solution 4: Unified Payment-to-Compliance Workflow

CashBook consolidates the entire expense lifecycle in one application:

Single App Experience:

Scan and pay at any UPI-enabled location

Instant invoice capture through photo upload

Expense categorization at the time of payment

Built-in approval workflows for managers

Real-time visibility for finance teams

This unified approach reduces documentation gaps by 80% compared to fragmented systems. Learn more about expense approval workflows that actually work.

Solution 5: Accounting System Integration

CashBook natively integrates with India's most-used accounting platforms:

Tally ERP integration for seamless ledger posting

Zoho Books synchronization for automated expense recording

Custom API connections for enterprise accounting systems

Every transaction flows directly into your financial records, eliminating manual data entry and reducing month-end close time by up to 71%.

Explore our Tally integration and Zoho Books integration.

Solution 6: Predictable, Flat Pricing Model

₹3,499 per wallet. That's it.

No percentage of transaction value

No scaling cost surprises as you grow

No hidden processing fees

Predictable annual budgeting

Whether your employee spends ₹10,000 or ₹5,00,000 monthly, your per-wallet cost remains constant. This pricing transparency enables accurate business spend management forecasting.

Solution 7: Industry-Specific Solutions

CashBook delivers tailored implementations for sector-specific challenges:

Construction industry expense management for site teams

Logistics company solutions for driver expenses

Manufacturing operations tracking

CashBook UPI Wallets: Understanding the Trade-Offs

Regulatory Requirement: KYC Compliance

Unlike e-RUPI's no-KYC model, CashBook requires:

Business KYC: Standard company verification documents

Employee KYC: Individual identity verification for wallet creation

Why This Matters:

While this adds initial setup time, KYC compliance provides:

Enhanced fraud prevention and security

Clear audit trails for regulatory requirements

Protection against misuse and financial crime

Compliance with RBI semi-closed wallet guidelines

For responsible company expense management, KYC verification represents a small upfront investment that delivers long-term governance benefits.

Comprehensive Comparison: e-RUPI vs CashBook UPI Wallets

Factor | e-RUPI Vouchers | CashBook UPI Wallets |

P2P Payment Support | ❌ Not supported | ✅ Fully supported |

P2M Payment Support | ✅ Supported (restricted) | ✅ Fully supported |

Merchant Enablement Required | ✅ Yes (major barrier) | ❌ No dependency |

MCC Classification Dependency | ✅ Yes (inconsistent) | ❌ No restriction |

Bank Account Restriction | Often required | No restriction |

Implementation Timeline | 4-8 weeks | 24-48 hours |

Invoice & Payment Workflow | Fragmented (multiple apps) | Unified (single app) |

Pricing Model | 0.5%-0.7% of GTV | ₹3,499 per wallet |

Employee KYC Requirement | Not required | Required |

Transaction Limits | ₹10,000-₹50,000 per voucher | Flexible (admin-controlled) |

Accounting Integration | Limited | Native (Tally, Zoho Books) |

Universal UPI Acceptance | ❌ No | ✅ Yes |

Real-Time Expense Visibility | Limited | Complete dashboard |

Mobile-First Approval Workflow | External apps | Built-in |

Real-World Use Case Scenarios: Which Solution Fits Your Business?

Scenario 1: Field Sales Team (15 Employees)

Business Need: Fuel, client meals, local travel, office supplies

e-RUPI Challenge:

Fuel pumps may be e-RUPI enabled ✓

Client restaurant meals likely restricted ✗

Auto-rickshaw rides (P2P) won't work ✗

Small stationery shops (P2P) excluded ✗

CashBook Solution: Universal acceptance across all vendor types. Single wallet handles diverse expense categories without fragmentation.

Read: Travel expense tracker solutions

Scenario 2: Construction Site Management (25 Workers)

Business Need: Hardware purchases, contractor payments, worker allowances, diesel

e-RUPI Challenge:

Local hardware vendors often use P2P ✗

On-site contractors require flexible payment ✗

Limited MCC categorization for construction supplies ✗

CashBook Solution: P2P capability essential for informal vendor network. Real-time tracking prevents leakage. Learn about construction imprest management.

Scenario 3: Growing Software Company (50 Employees)

Business Need: Co-working space payments, SaaS subscriptions, team events, client meetings

e-RUPI Challenge:

Vendor payment limits create splits ✗

Monthly subscription handling complex ✗

Co-working spaces may lack e-RUPI ✗

CashBook Solution: Flexible limits accommodate larger transactions. Accounting integration automates expense categorization for tax compliance.

Compare with best business expense management apps.

Making the Right Decision: Expert Recommendations for CFOs and Finance Leaders

The choice between e-RUPI and CashBook UPI Wallets isn't about "better" or "worse"; it's about alignment with operational reality.

Choose e-RUPI When:

Running targeted benefit programs with specific redemption partners

Distributing welfare benefits where merchant control is essential

Managing government-backed schemes requiring purpose restrictions

Operating in highly controlled ecosystems with limited vendor diversity

Choose CashBook UPI Wallets When:

Managing distributed field teams across diverse geographies

Dealing with hybrid merchant networks (formal + informal)

Requiring rapid deployment for growing operations

Needing accounting system integration for compliance

Seeking predictable costs that don't scale with transaction volume

Operating in industries with P2P-heavy spending patterns

Industry-Specific Considerations for Expense Management Solutions

Manufacturing & Production

Production floors involve constant small-value purchases from local suppliers. Manufacturing expense tracking requires P2P flexibility for informal vendor payments.

Logistics & Transportation

Driver expenses, toll payments, and roadside vendor transactions occur predominantly via P2P channels. Logistics expense management demands universal acceptance.

Hospitality & Food Services

Multi-outlet restaurant operations need centralized visibility with location-specific controls; difficult with fragmented e-RUPI vouchers.

Professional Services

Consulting firms require flexible business central expense management that accommodates client-facing spending without merchant restrictions.

The Bottom Line: Flexibility Wins in India's Payment Ecosystem

After analyzing 3,000+ business implementations and processing over ₹500 crore in employee expense reimbursements, one conclusion emerges consistently:

India's business spending happens in a hybrid ecosystem; and your expense management solution must reflect that reality.

e-RUPI represents impressive innovation for targeted benefit distribution. Its purpose-specific architecture serves government programs and controlled benefit schemes effectively.

But corporate expense management demands different priorities:

Acceptance flexibility over merchant restriction

Operational speed over implementation complexity

Unified workflows over fragmented experiences

P2P capability over P2M-only architecture

Accounting integration over standalone vouchers

CashBook UPI Wallets emerged specifically to address these real-world needs. We didn't start with theory about what businesses should need; we analyzed how they actually spend.

Take Action: Evaluate Your Expense Management Needs

Key Questions for Decision-Makers:

What percentage of your employee expenses occur at informal vendors using P2P?

If >30%, e-RUPI creates significant acceptance issues

How quickly do you need to deploy a solution?

If <2 weeks, e-RUPI's implementation timeline may not fit

Do your employees travel to diverse locations with unpredictable vendor types?

If yes, universal UPI acceptance becomes critical

Are accounting system integrations important for your compliance processes?

If yes, CashBook's native integrations provide significant value

Is predictable cost budgeting a priority as you scale?

If yes, flat per-wallet pricing prevents cost surprises

Next Steps: Experience CashBook UPI Wallets

For businesses ready to modernize employee expense management:

Book a 10-minute demo to see CashBook in action

Start a free trial with 5 wallets (no credit card required)

Review case studies from your industry

Calculate potential savings with our ROI calculator

The future of business expense management in India isn't about theoretical control; it's about practical solutions that work where your employees actually transact.

CashBook makes expense management simple, compliant, and built for India's real payment ecosystem.

Frequently Asked Questions

What is e-RUPI and how does it work for business expenses in India?

e-RUPI is a prepaid, purpose-specific digital voucher launched by NPCI. It works by locking funds to specific merchants or Merchant Category Codes (MCCs), meaning employees can only redeem vouchers at pre-approved, bank-enabled P2M (Person-to-Merchant) terminals. While useful for targeted benefit programs like fuel or medical allowances, e-RUPI cannot process P2P payments, which account for over 55% of real-world business expenses in India, including local vendors, auto drivers, and construction site suppliers.

Why does e-RUPI not work at local vendors and small shops in India?

e-RUPI only supports P2M (Person-to-Merchant) transactions at formally registered, bank-enabled merchant terminals. Most local hardware shops, auto-rickshaw drivers, construction site vendors, small grocery stores, and on-demand service providers in India transact via personal UPI IDs (P2P), which e-RUPI cannot process. Additionally, even formal merchants with QR codes may reject e-RUPI if their acquiring bank has not enabled e-RUPI processing or if their Merchant Category Code is incorrectly classified, which is a common problem across India's banking network.

What is the difference between e-RUPI and CashBook UPI Wallets for employee expense management?

The core difference is payment universality. e-RUPI is restricted to P2M merchants with specific bank enablement and MCC classification, charges 0.5 to 0.7% of transaction value, takes 4 to 8 weeks to implement, and splits payment, invoice, and reporting across multiple apps. CashBook UPI Wallets work across all 55+ million UPI QR codes including P2P payments, charge a flat Rs. 3,499 per wallet annually with no per-transaction fees, deploy in 24 to 48 hours, and unify payment, bill upload, approval, and accounting sync in a single app.

Is e-RUPI suitable for field sales teams and construction site expenses?

No. e-RUPI is poorly suited for field teams because the majority of their spending happens at informal vendors using P2P QR codes, including fuel from local pumps, meals at roadside dhabas, materials from hardware shops, and payments to auto drivers, none of which e-RUPI can process. For field operations, CashBook UPI Wallets are a better fit as they support both P2P and P2M payments universally, with real-time spend controls, geo-tagged receipts, and manager-controlled wallet limits.

How does e-RUPI pricing compare to CashBook at scale?

e-RUPI charges 0.5 to 0.7% of gross transaction value, which scales linearly with business growth. A company spending Rs. 5 crore annually pays Rs. 2.5 lakh in provider fees; at Rs. 20 crore in annual expenses, that becomes Rs. 10 lakh per year purely in transaction fees. CashBook charges a flat Rs. 3,499 per wallet per year regardless of how much is spent through it, making costs fully predictable and independent of transaction volume.

When should a business choose e-RUPI over CashBook UPI Wallets?

e-RUPI is the right choice for targeted, controlled benefit distribution such as government scholarship programs, corporate welfare benefits like gym memberships or health insurance, vendor-locked payments to specific service providers, or subsidy programs requiring strict redemption restrictions. It is not suited for general corporate expense management with diverse, field-based, or informal vendor spending. CashBook UPI Wallets are better when teams need universal payment acceptance, rapid deployment, accounting integration, and predictable pricing that does not scale with transaction volume.